Zero-based Monthly Budget Spreadsheet

A zero-based monthly budget spreadsheet is a powerful tool for taking control of your finances. The core concept is simple: you allocate every single dollar you earn to a specific purpose, ensuring that your income minus your expenses equals zero. This doesn’t mean you have no money left at the end of the month; instead, it means every dollar is intentionally assigned, whether it’s to bills, savings, debt repayment, or discretionary spending.

This approach forces you to be mindful of where your money is going and proactively plan for all your expenses. Unlike traditional budgeting methods that track spending after the fact, a zero-based budget is created before the month begins, allowing you to anticipate and prioritize your financial goals. This prospective planning is crucial for achieving financial stability, reducing debt, and building wealth.

Benefits of a Zero-Based Budget Spreadsheet

Implementing a zero-based budget spreadsheet offers numerous advantages:

- Increased Awareness: It provides a clear picture of your income, expenses, and where your money is truly going. This awareness empowers you to make informed financial decisions.

- Prioritization of Goals: By allocating funds to specific savings goals (e.g., emergency fund, down payment, retirement), you ensure that your financial priorities are being met.

- Debt Reduction: You can strategically allocate extra funds towards debt repayment, accelerating the process of becoming debt-free.

- Reduced Overspending: The act of assigning every dollar makes you more conscious of your spending habits, reducing impulsive purchases and unnecessary expenses.

- Proactive Financial Planning: Planning your budget in advance allows you to anticipate upcoming expenses and avoid financial surprises.

- Flexibility and Control: While the initial budget requires careful planning, it can be adjusted throughout the month as needed, providing you with greater control over your finances.

- Improved Financial Stability: Consistently using a zero-based budget fosters responsible financial habits and promotes long-term financial stability.

Creating Your Zero-Based Budget Spreadsheet

While dedicated budgeting apps are available, a simple spreadsheet (using Google Sheets, Microsoft Excel, or similar software) is often the best place to start. Here’s a step-by-step guide to building your own:

- Open Your Spreadsheet Software: Launch your preferred spreadsheet program.

- Create Headings: In the first row, create the following headings:

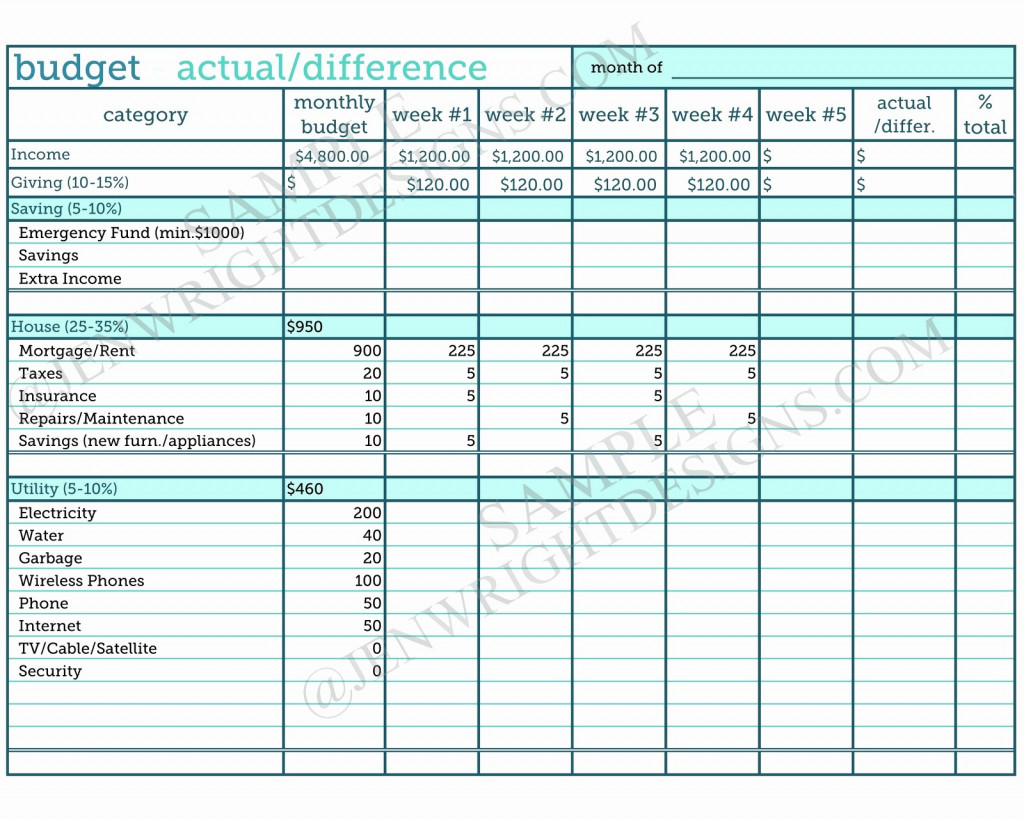

- Category: This column will list your different income and expense categories.

- Expected Income/Expense: This is the amount you expect to receive or spend in each category.

- Actual Income/Expense: This is the actual amount you receive or spend.

- Difference: This column will calculate the difference between your expected and actual amounts.

- Notes: (Optional) This column can be used to add notes or details about specific transactions.

- List Your Income Sources: Under the “Category” column, list all sources of income you expect to receive during the month. This could include your salary, freelance income, investment income, or any other recurring income. Be realistic with your income projections. It’s better to underestimate slightly than to overestimate.

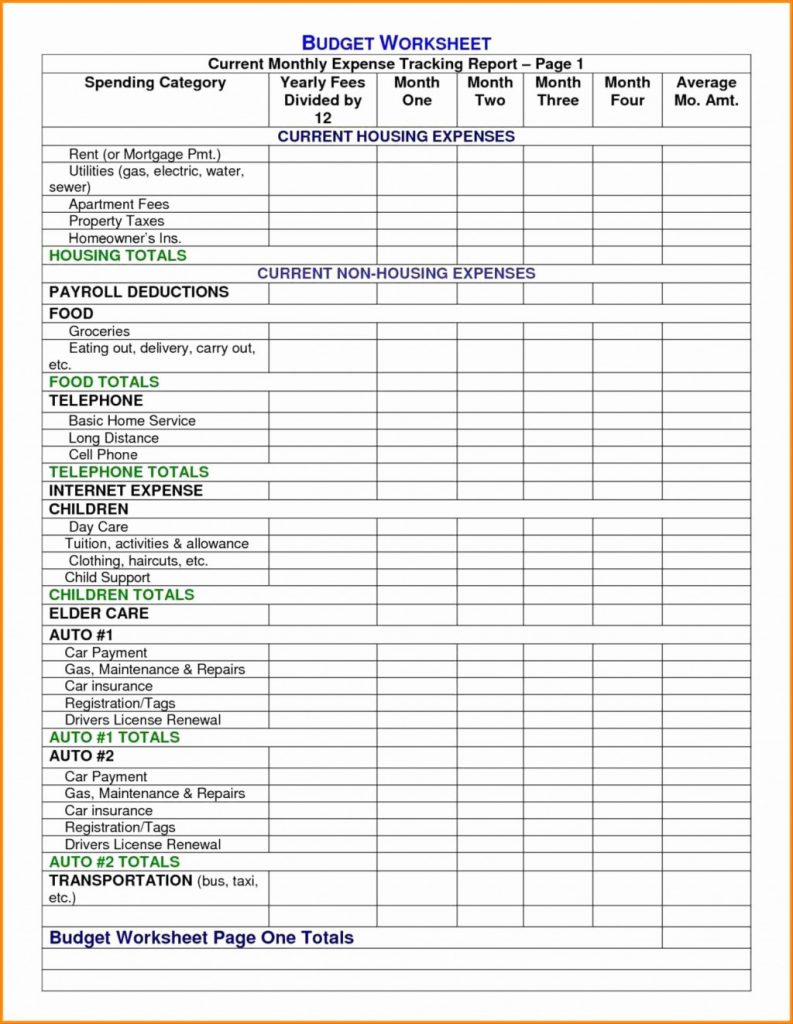

- List Your Expenses: Underneath your income sources, list all your expected expenses for the month. Divide these expenses into categories such as:

- Housing: Rent or mortgage payments, property taxes, homeowner’s insurance.

- Utilities: Electricity, gas, water, internet, phone.

- Transportation: Car payments, gas, insurance, public transportation.

- Food: Groceries, dining out.

- Debt Payments: Credit card payments, student loan payments, personal loans.

- Insurance: Health insurance, life insurance.

- Savings: Emergency fund, retirement contributions, other savings goals.

- Personal Care: Haircuts, toiletries, gym memberships.

- Entertainment: Movies, concerts, subscriptions.

- Clothing: New clothes, shoes.

- Miscellaneous: Unforeseen expenses, gifts.

- Estimate Expected Income and Expenses: For each income source and expense category, enter your expected amount in the “Expected Income/Expense” column. Use your past spending records, bank statements, and receipts to make accurate estimates. If you have variable expenses (like groceries), estimate on the higher side to avoid surprises.

- Calculate Total Expected Income and Expenses: At the bottom of the income section, use the SUM function to calculate your total expected income. Similarly, calculate your total expected expenses at the bottom of the expense section.

- Ensure Zero Balance: Subtract your total expected expenses from your total expected income. The result should be zero. If it’s not, you need to adjust your budget. Identify areas where you can reduce spending or reallocate funds to ensure that every dollar is accounted for. This is the core principle of a zero-based budget.

- Track Actual Income and Expenses: Throughout the month, diligently track your actual income and expenses. As you receive income or make a purchase, enter the actual amount in the “Actual Income/Expense” column next to the corresponding category.

- Calculate the Difference: Use a formula to calculate the difference between your expected and actual amounts in the “Difference” column. For example, if your expected grocery expense was $400 and your actual expense was $450, the difference would be -$50. This will highlight areas where you are overspending or underspending. The formula would be `=Actual Income/Expense – Expected Income/Expense`.

- Analyze and Adjust: At the end of the month, review your spreadsheet and analyze the differences between your expected and actual amounts. Identify areas where you consistently overspend or underspend. Based on this analysis, adjust your budget for the following month. For instance, if you consistently overspend on dining out, you may need to reduce your allocated amount for that category.

Tips for Success

Here are some tips to help you succeed with your zero-based budget:

- Be Realistic: Don’t underestimate your expenses or overestimate your income. Be honest about your spending habits and financial situation.

- Review Regularly: Review your budget spreadsheet regularly (ideally weekly or even daily) to track your progress and make adjustments as needed.

- Categorize Expenses Carefully: Choose expense categories that are meaningful to you and that accurately reflect your spending habits.

- Embrace Flexibility: Life happens, and unexpected expenses will arise. Be prepared to adjust your budget as needed to accommodate these surprises. However, make sure that every adjustment maintains the zero-based principle, meaning that you reallocate funds from another category to cover the unforeseen expense.

- Automate Savings: Set up automatic transfers to your savings accounts to ensure that you consistently reach your savings goals.

- Consider “Sinking Funds”: Sinking funds are designated savings accounts for specific future expenses, such as holiday gifts, car repairs, or vacations. Creating sinking funds helps you avoid going into debt for these predictable expenses.

- Don’t Get Discouraged: It takes time to develop a successful budgeting habit. Don’t get discouraged if you make mistakes or encounter challenges along the way. The key is to learn from your experiences and keep improving your budgeting skills.

Example Categories for Your Spreadsheet

To further illustrate how to set up your spreadsheet, here’s a more detailed list of potential income and expense categories:

Income:

- Salary (Net Pay)

- Freelance Income

- Investment Income (Dividends, Interest)

- Rental Income

- Side Hustle Income

- Tax Refunds

Expenses:

- Housing:

- Rent/Mortgage Payment

- Property Taxes

- Homeowner’s/Renter’s Insurance

- HOA Fees

- Maintenance/Repairs

- Utilities:

- Electricity

- Gas

- Water/Sewer/Trash

- Internet

- Phone (Cell and/or Landline)

- Cable/Satellite TV (if applicable)

- Transportation:

- Car Payment(s)

- Car Insurance

- Gasoline

- Car Maintenance/Repairs

- Public Transportation (Bus, Train)

- Parking Fees

- Tolls

- Food:

- Groceries

- Dining Out

- Coffee/Snacks

- Debt Payments:

- Credit Card Payments

- Student Loan Payments

- Personal Loan Payments

- Car Loan Payment

- Mortgage Payment (already included in Housing)

- Insurance:

- Health Insurance Premium

- Life Insurance Premium

- Dental Insurance Premium

- Vision Insurance Premium

- Savings:

- Emergency Fund

- Retirement Contributions (401k, IRA)

- Down Payment Fund

- Vacation Fund

- Education Fund (for yourself or children)

- Sinking Funds (Holiday Gifts, Car Repairs, etc.)

- Personal Care:

- Haircuts/Styling

- Toiletries

- Gym Membership

- Spa Treatments

- Cosmetics

- Entertainment:

- Movies

- Concerts

- Sporting Events

- Streaming Subscriptions (Netflix, Spotify, etc.)

- Books/Magazines

- Hobbies

- Clothing:

- New Clothes

- Shoes

- Accessories

- Laundry/Dry Cleaning

- Gifts/Charity:

- Birthday Gifts

- Holiday Gifts

- Wedding Gifts

- Charitable Donations

- Medical Expenses:

- Doctor Visits

- Prescriptions

- Over-the-Counter Medications

- Dental Care

- Vision Care

- Miscellaneous:

- Bank Fees

- Postage/Shipping

- Pet Care

- Subscriptions (other than streaming services)

- Unforeseen Expenses

By taking the time to create and consistently use a zero-based monthly budget spreadsheet, you can gain control of your finances, achieve your financial goals, and build a more secure future. Remember that it’s a process, and it requires dedication and discipline, but the rewards are well worth the effort.

793×1024 based budget spreadsheet based budget spreadsheet from db-excel.com

793×1024 based budget spreadsheet based budget spreadsheet from db-excel.com  601×797 based budget spreadsheet intended based budget from db-excel.com

601×797 based budget spreadsheet intended based budget from db-excel.com  1000×1500 based budget spreadsheet healthy wealthy skinny from www.healthywealthyskinny.com

1000×1500 based budget spreadsheet healthy wealthy skinny from www.healthywealthyskinny.com  794×596 based budget spreadsheet monthly budget planner excel etsy from www.etsy.com

794×596 based budget spreadsheet monthly budget planner excel etsy from www.etsy.com  1024×819 based budget spreadsheet db excelcom from db-excel.com

1024×819 based budget spreadsheet db excelcom from db-excel.com

Zero-based Monthly Budget Spreadsheet :

Zero-based Monthly Budget Spreadsheet was posted in October 19, 2025 at 1:06 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Zero-based Monthly Budget Spreadsheet Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!

Related For Zero-based Monthly Budget Spreadsheet

Monthly Financial Budget Template

Monthly Financial Budget Template Letter Of Authorization PDFThank You

Commission-based Income Budget Plan

“`html Commission-Based Income Budget Planner Budgeting with a stable,

Business Budget for Multiple Produc

Business Budget for Multiple Products Sample Excel Format Personal