Fixed Income Budget Worksheet For Retirees

Fixed Income Budget Worksheet for Retirees

Retirement often brings a significant shift in income sources. Relying primarily on fixed income requires meticulous budgeting and financial planning to ensure a comfortable and secure lifestyle. This worksheet provides a structured approach to creating a fixed income budget, tailored for retirees.

Why a Fixed Income Budget is Crucial

A well-defined budget helps retirees:

- Maintain Financial Stability: By tracking income and expenses, you can ensure your fixed income covers your needs and avoid overspending.

- Identify Spending Patterns: Understanding where your money goes allows you to identify areas for potential cost savings.

- Plan for Unexpected Expenses: A budget helps allocate funds for emergencies and unexpected healthcare costs, which are common in retirement.

- Achieve Financial Goals: Even in retirement, you may have goals like travel, hobbies, or helping family. A budget helps you save and allocate funds towards these aspirations.

- Reduce Financial Stress: Knowing where you stand financially provides peace of mind and reduces anxiety about money.

Worksheet Structure

This worksheet is divided into sections to help you comprehensively assess your income and expenses. It’s recommended to complete each section thoroughly and review your budget regularly (at least quarterly) to make necessary adjustments.

I. Income Assessment

List all sources of fixed income you receive regularly. Be as precise as possible and consider both gross and net income (after taxes and other deductions, if applicable).

| Income Source | Gross Monthly Amount | Net Monthly Amount |

|---|---|---|

| Social Security | ||

| Pension(s) | ||

| Annuities | ||

| Interest from Savings/Investments | ||

| Dividends from Investments | ||

| Rental Income (Net) | ||

| Part-Time Employment (Net) | ||

| Other Income (Specify): | ||

| Total Monthly Income |

Important Notes:

- Net vs. Gross: Use net income (after taxes and deductions) for the most accurate picture of your spendable income.

- Tax Implications: Be mindful of the tax implications of different income sources. Some income, like Social Security, may be taxable.

- Inflation Adjustment: Consider how inflation might affect your income over time, especially for fixed pensions or annuities.

II. Expense Tracking

Categorize your monthly expenses and estimate the amount you spend in each category. Use your bank statements, credit card statements, and receipts to get accurate figures. Divide expenses into fixed (consistent each month) and variable (fluctuating). If you pay expenses annually or quarterly, divide the total amount by 12 to get a monthly equivalent.

| Expense Category | Fixed Monthly Amount | Variable Monthly Amount | Notes |

|---|---|---|---|

| Housing: | |||

| Mortgage/Rent | |||

| Property Taxes | Calculate monthly equivalent | ||

| Homeowner’s Insurance | Calculate monthly equivalent | ||

| Home Maintenance/Repairs | Estimate average monthly spending | ||

| HOA Fees | |||

| Utilities: | |||

| Electricity | |||

| Gas/Heating Oil | |||

| Water/Sewer | |||

| Trash/Recycling | |||

| Internet | |||

| Cable/Satellite TV | |||

| Phone (Landline/Cell) | |||

| Food & Groceries: | |||

| Groceries | |||

| Dining Out | |||

| Transportation: | |||

| Car Payment (if applicable) | |||

| Car Insurance | Calculate monthly equivalent | ||

| Gasoline | |||

| Car Maintenance/Repairs | Estimate average monthly spending | ||

| Public Transportation | |||

| Healthcare: | |||

| Health Insurance Premiums | |||

| Prescription Medications | |||

| Doctor Visits/Co-pays | |||

| Dental Care | |||

| Vision Care | |||

| Insurance (Other): | |||

| Life Insurance | |||

| Long-Term Care Insurance | |||

| Personal Care: | |||

| Clothing | |||

| Haircuts/Grooming | |||

| Entertainment & Recreation: | |||

| Hobbies | |||

| Travel | Calculate monthly equivalent from annual budget | ||

| Movies/Concerts/Events | |||

| Gifts & Donations: | |||

| Gifts (Birthdays, Holidays) | |||

| Charitable Donations | |||

| Debt Payments: | |||

| Credit Card Payments | |||

| Loans (Personal, Student, etc.) | |||

| Miscellaneous: | |||

| Pet Care | |||

| Subscriptions (Magazines, Streaming Services) | |||

| Bank Fees | |||

| Other Expenses (Specify): | |||

| Total Monthly Expenses |

Important Notes:

- Be Thorough: Don’t underestimate any expense category. Even small amounts can add up.

- Average Variable Expenses: For variable expenses, calculate an average monthly amount based on past spending habits.

- Annual Expenses: Convert annual or quarterly expenses to a monthly equivalent for a consistent view.

- Contingency Fund: Include a line item for a contingency fund to cover unexpected expenses.

III. Budget Analysis

Now, compare your total monthly income to your total monthly expenses:

- Total Monthly Income: (From Section I)

- Total Monthly Expenses: (From Section II)

- Monthly Surplus/Deficit: (Income – Expenses)

Interpreting the Results:

- Surplus: If your income exceeds your expenses, you have a surplus. You can allocate this surplus towards savings, investments, or discretionary spending.

- Deficit: If your expenses exceed your income, you have a deficit. This requires immediate attention to reduce expenses or increase income.

- Balanced Budget: Ideally, you want a budget that is close to balanced, with a slight surplus for unexpected expenses or future goals.

IV. Action Plan: Addressing a Deficit or Optimizing a Surplus

If you have a deficit:

- Identify Areas to Cut: Review your expense categories and identify areas where you can reduce spending. Focus on non-essential expenses first. Consider cutting back on dining out, entertainment, subscriptions, or travel.

- Negotiate Lower Rates: Contact your service providers (insurance, internet, phone) to negotiate lower rates. Shop around for better deals.

- Reduce Housing Costs: If housing costs are a significant portion of your expenses, consider downsizing or refinancing your mortgage (if applicable).

- Increase Income (if possible): Explore opportunities for part-time employment or consulting work. Consider selling unused assets.

- Prioritize Debt Payments: Focus on paying down high-interest debt to reduce your monthly payments.

If you have a surplus:

- Build an Emergency Fund: Ensure you have 3-6 months’ worth of living expenses in an easily accessible savings account.

- Invest for the Future: Consider investing a portion of your surplus to grow your wealth and protect against inflation. Consult with a financial advisor.

- Pay Down Debt: Accelerate your debt repayment to save on interest and free up cash flow in the future.

- Enjoy Your Retirement: Allocate a portion of your surplus towards hobbies, travel, or other activities you enjoy.

- Plan for Future Expenses: Set aside funds for future expenses, such as home repairs or healthcare costs.

V. Regular Review and Adjustment

Your budget is not a one-time task. It’s an ongoing process that requires regular review and adjustment. At least quarterly, review your actual income and expenses against your budgeted amounts. Identify any discrepancies and make necessary adjustments to your budget. Life circumstances can change, impacting your income and expenses. Stay proactive in managing your finances to ensure a comfortable and secure retirement.

Tips for Successful Budgeting:

- Use Budgeting Tools: Utilize budgeting apps or software to track your income and expenses automatically.

- Automate Savings: Set up automatic transfers to your savings account each month.

- Be Realistic: Create a budget that is realistic and sustainable for your lifestyle.

- Seek Professional Advice: Consult with a financial advisor to get personalized guidance on retirement planning and budgeting.

- Stay Disciplined: Stick to your budget as closely as possible to achieve your financial goals.

By using this fixed income budget worksheet and following these tips, retirees can gain control of their finances, ensure financial stability, and enjoy a fulfilling retirement.

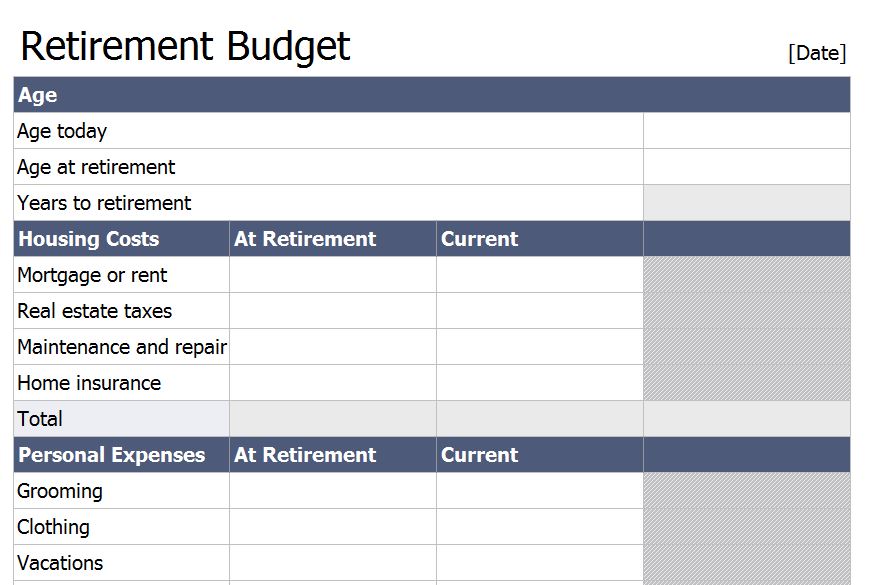

1000×1294 retirement budget spreadsheet db excelcom from db-excel.com

1000×1294 retirement budget spreadsheet db excelcom from db-excel.com  1285×1660 retirement budget worksheet db excelcom from db-excel.com

1285×1660 retirement budget worksheet db excelcom from db-excel.com  390×505 retirement budget worksheet templates from www.template.net

390×505 retirement budget worksheet templates from www.template.net  870×585 retirement budget worksheet retirement budget template template haven from templatehaven.com

870×585 retirement budget worksheet retirement budget template template haven from templatehaven.com  601×778 retirement budget spreadsheet retirement budget spreadsheet from db-excel.com

601×778 retirement budget spreadsheet retirement budget spreadsheet from db-excel.com

Fixed Income Budget Worksheet For Retirees :

Fixed Income Budget Worksheet For Retirees was posted in November 8, 2025 at 3:33 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Fixed Income Budget Worksheet For Retirees Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!

Related For Fixed Income Budget Worksheet For Retirees

Home Budget Template PDF Format Dow

Home Budget Template PDF Format Download Training Survey Template

Example Vacation Budget Spreadsheet

Example Vacation Budget Spreadsheet Template PDF Download Notice LetterSolopreneur Budget Tracker Spreadsh

Here’s an HTML document outlining a solopreneur budget tracker