Student Life Budgeting Kit

Student Life Budgeting Kit: Survive and Thrive

Navigating student life involves juggling lectures, assignments, social events, and, crucially, finances. This guide provides a comprehensive budgeting kit to help you manage your money effectively, reduce stress, and build healthy financial habits for the future.

Why Budgeting is Essential for Students

Student life often comes with limited income and significant expenses. Without a budget, it’s easy to overspend, accumulate debt, and feel overwhelmed by financial anxieties. A well-structured budget offers several benefits:

- Financial Awareness: Understand where your money is going, identifying spending patterns and areas for potential savings.

- Debt Avoidance: Prevent unnecessary debt accumulation by living within your means.

- Goal Setting: Enables you to save for specific goals, like travel, a new laptop, or future investments.

- Reduced Stress: Gain control over your finances, alleviating stress related to money management.

- Financial Literacy: Develop valuable money management skills that will benefit you throughout your life.

The Student Budgeting Kit: A Step-by-Step Guide

Step 1: Track Your Income

Identify all your sources of income. Be realistic and include only regular and reliable sources. Common income sources for students include:

- Student Loans: Calculate the net amount after tuition fees and other mandatory deductions.

- Grants and Scholarships: Include any grants or scholarships you receive.

- Part-Time Jobs: Estimate your average monthly earnings from your part-time job.

- Allowance from Parents/Guardians: If you receive financial support, include the regular amount.

- Savings: If you’re drawing from a savings account, include the monthly amount.

Create a simple spreadsheet or use a budgeting app to list all your income sources and their respective amounts. This provides a clear picture of your available funds.

Step 2: Identify Your Expenses

Categorize your expenses into two main groups: fixed and variable.

Fixed Expenses:

These expenses remain relatively constant each month and are predictable. Examples include:

- Rent/Housing: Monthly rent payment or dorm fees.

- Utilities: Electricity, water, gas, and internet bills.

- Tuition Fees (if not covered by loans): Any remaining tuition fees you need to pay.

- Transportation: Bus passes, train tickets, or car payments (including insurance and fuel).

- Phone Bill: Monthly mobile phone plan costs.

- Insurance: Health insurance, renter’s insurance (if applicable).

Variable Expenses:

These expenses fluctuate from month to month and require careful tracking. Examples include:

- Groceries: Food and household supplies.

- Eating Out/Takeaway: Meals at restaurants or takeaway orders.

- Entertainment: Movies, concerts, social gatherings, hobbies.

- Books and Supplies: Textbooks, stationery, and other academic materials.

- Personal Care: Toiletries, haircuts, clothing.

- Miscellaneous: Unexpected expenses, gifts, subscriptions.

To accurately track variable expenses, consider using:

- Budgeting Apps: Apps like Mint, YNAB (You Need A Budget), or PocketGuard automatically track your spending by linking to your bank accounts.

- Spreadsheets: Manually record your expenses in a spreadsheet, categorizing each transaction.

- Note-Taking Apps: Use a note-taking app on your phone to jot down expenses as you make them.

Track your expenses for at least a month to get a clear understanding of your spending habits.

Step 3: Create Your Budget

Now that you know your income and expenses, it’s time to create your budget. Use the following equation:

Total Income – Total Expenses = Net Income (or Deficit)

Ideally, you want a positive net income (surplus). If you have a deficit, you need to adjust your spending to bring your expenses in line with your income.

Allocate your income to different expense categories based on your needs and priorities. Here are some budgeting methods you can use:

- 50/30/20 Rule: Allocate 50% of your income to needs (essential expenses like rent, groceries, and transportation), 30% to wants (entertainment, dining out, hobbies), and 20% to savings and debt repayment.

- Zero-Based Budgeting: Allocate every dollar of your income to a specific category, ensuring that your income minus your expenses equals zero. This method requires meticulous planning but can be very effective.

- Envelope System: Allocate cash to different expense categories and place the cash in labeled envelopes. Once the envelope is empty, you can’t spend any more money in that category until the next budgeting period. This method is particularly helpful for controlling variable expenses.

Adjust your budget as needed to reflect your actual spending habits. Review your budget regularly (weekly or monthly) to identify areas where you can save money or make adjustments.

Step 4: Implement Saving Strategies

Saving money is crucial for achieving your financial goals and building a financial safety net. Here are some saving strategies for students:

- Set Savings Goals: Define specific savings goals, such as saving for a textbook, a trip, or an emergency fund. Having clear goals will motivate you to save.

- Automate Savings: Set up automatic transfers from your checking account to your savings account each month. Even small, regular contributions can add up over time.

- Reduce Expenses: Identify areas where you can cut back on spending. Consider cooking more meals at home, finding free entertainment options, or using student discounts.

- Find Affordable Housing: Explore options like living with roommates or finding cheaper accommodation.

- Buy Used Textbooks: Save money by purchasing used textbooks or renting them from the library.

- Utilize Student Discounts: Take advantage of student discounts offered at various businesses, such as movie theaters, museums, and restaurants.

- Avoid Unnecessary Subscriptions: Evaluate your subscriptions and cancel any that you don’t use regularly.

- Limit Eating Out: Prepare your own meals whenever possible to avoid the higher costs of eating out.

- Pack Your Lunch: Bringing your own lunch to campus can save you a significant amount of money compared to buying lunch every day.

- Brew Coffee at Home: Making your own coffee instead of buying it at a coffee shop can save you a lot of money over time.

Step 5: Manage Debt Wisely

Debt can be a major burden, especially for students. Manage your debt responsibly by following these tips:

- Avoid Credit Card Debt: Use credit cards responsibly and pay off your balance in full each month to avoid high interest charges.

- Minimize Student Loan Debt: Borrow only what you need and explore options for repayment assistance programs.

- Prioritize Debt Repayment: If you have multiple debts, prioritize paying off the ones with the highest interest rates first.

- Explore Debt Consolidation Options: Consider consolidating your debts into a single loan with a lower interest rate.

Step 6: Review and Adjust Regularly

Your budget is not a static document. It’s essential to review and adjust it regularly to reflect changes in your income, expenses, and financial goals. Make it a habit to review your budget weekly or monthly to stay on track and make necessary adjustments.

Essential Tools for Student Budgeting

- Budgeting Apps: Mint, YNAB (You Need A Budget), PocketGuard, Personal Capital.

- Spreadsheet Software: Microsoft Excel, Google Sheets.

- Banking Apps: Your bank’s mobile app for tracking transactions.

- Financial Calculators: Online calculators for loan repayment, savings goals, and investment returns.

942×660 student budget planner infographic from blog.optimal-partners.com

942×660 student budget planner infographic from blog.optimal-partners.com  750×875 student budget templates saving tips from www.wordtemplatesonline.net

750×875 student budget templates saving tips from www.wordtemplatesonline.net  1200×627 create student budget sdn from www.studentdoctor.net

1200×627 create student budget sdn from www.studentdoctor.net  680×870 student budget templates word documents from www.template.net

680×870 student budget templates word documents from www.template.net  600×730 student budget templates sample format from www.template.net

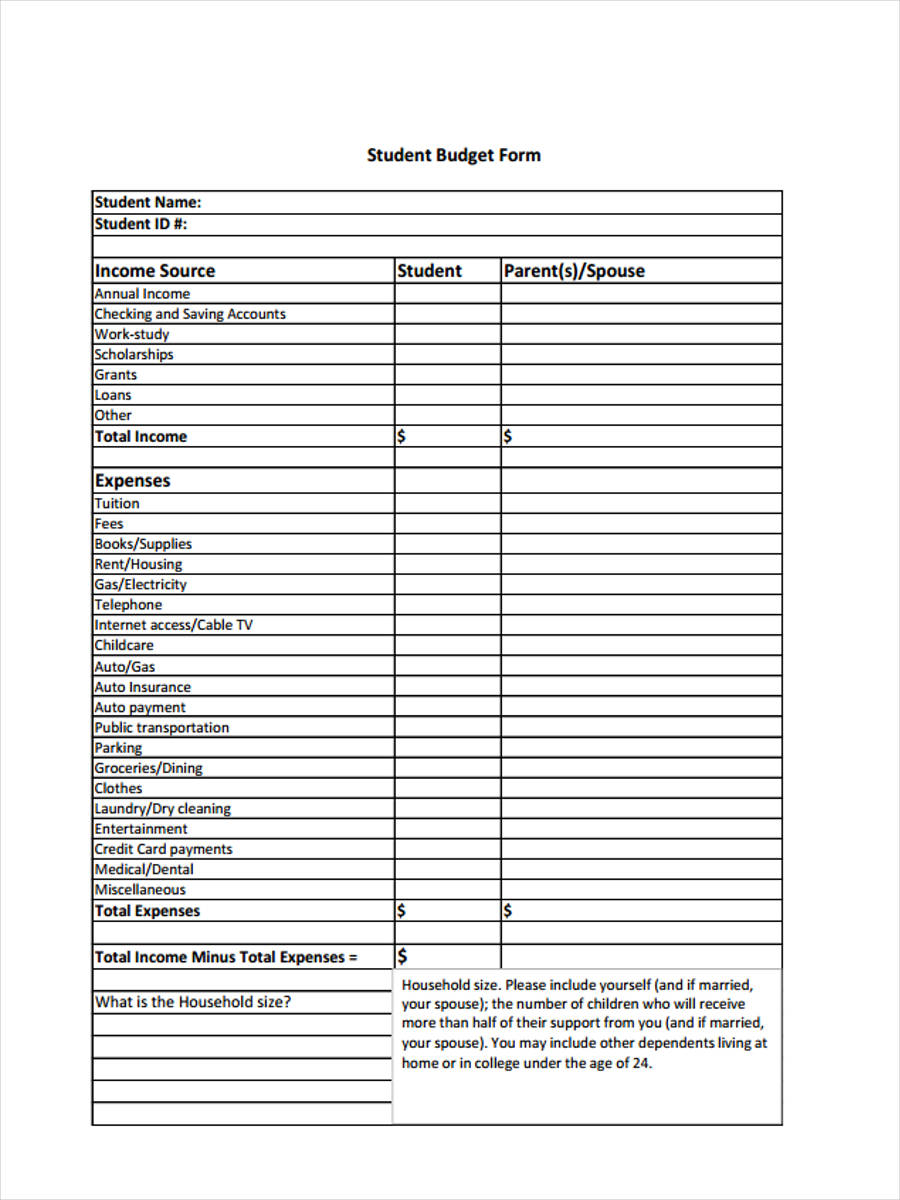

600×730 student budget templates sample format from www.template.net  900×1200 student budget forms ms word from www.sampleforms.com

900×1200 student budget forms ms word from www.sampleforms.com  1140×1140 printable teenager budget kit monthly income expenses tracking from www.etsy.com

1140×1140 printable teenager budget kit monthly income expenses tracking from www.etsy.com  2550×3300 student program budget templates allbusinesstemplatescom from www.allbusinesstemplates.com

2550×3300 student program budget templates allbusinesstemplatescom from www.allbusinesstemplates.com

Student Life Budgeting Kit :

Student Life Budgeting Kit was posted in December 16, 2025 at 4:06 pm. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Student Life Budgeting Kit Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!

Related For Student Life Budgeting Kit

Printable Wedding Budget Template P

Printable Wedding Budget Template PDF Download College Scholarship ThankApple Numbers Budget Spreadsheet

Apple Numbers: Your Guide to Budgeting Bliss Apple Numbers,Sample Wedding Budget Template

Sample Wedding Budget Template Termination of Medical Services Letter