Budgeting Plan Template For Retirement

Crafting Your Golden Years: A Retirement Budgeting Plan Template

Retirement. The word evokes images of leisurely mornings, pursuing long-held hobbies, and spending quality time with loved ones. However, the reality of a fulfilling retirement hinges on careful financial planning, particularly a robust budgeting plan. This template provides a framework to help you create a personalized retirement budget and navigate your financial future with confidence.

Understanding the Importance of a Retirement Budget

A retirement budget is more than just tracking expenses; it’s a roadmap to ensuring your financial independence and security during your post-working life. It allows you to:

- Assess Retirement Readiness: Determine if your current savings and projected income are sufficient to cover your desired lifestyle.

- Identify Potential Shortfalls: Pinpoint areas where you may need to cut back on spending or increase savings.

- Make Informed Decisions: Guides investment strategies and withdrawal plans.

- Maintain Financial Stability: Prevents overspending and ensures you can meet your essential needs.

- Reduce Stress: Provides peace of mind knowing your finances are under control.

Retirement Budgeting Plan Template: A Step-by-Step Guide

This template is designed to be flexible and adaptable to your unique circumstances. Feel free to adjust the categories and amounts to accurately reflect your individual situation.

Phase 1: Income Assessment

The first step is to identify all sources of income you expect to receive during retirement.

- Social Security: Obtain an estimated benefit statement from the Social Security Administration website (ssa.gov). Note that this is an estimate, and your actual benefit may vary.

- Pension Income: If you have a pension from a former employer, determine the amount you will receive monthly or annually. Understand the terms of the pension (e.g., survivor benefits, cost-of-living adjustments).

- Retirement Account Withdrawals (401(k), IRA, Roth IRA): Estimate your annual withdrawals from these accounts. Consider the tax implications of each type of account. It’s prudent to consult a financial advisor to develop a sustainable withdrawal strategy.

- Annuities: If you own an annuity, factor in the guaranteed income stream it provides.

- Part-Time Work or Consulting: If you plan to work part-time or offer consulting services, estimate your potential earnings.

- Rental Income: If you own rental properties, include the net rental income after deducting expenses.

- Investment Income (Dividends, Interest): Factor in income from investments such as stocks, bonds, and mutual funds.

- Other Income: Include any other sources of income, such as royalties, inheritance, or support from family members.

Total Estimated Annual Income: Sum up all the income sources listed above.

Phase 2: Expense Estimation

Next, estimate your expenses during retirement. Be as detailed as possible, breaking down your spending into categories.

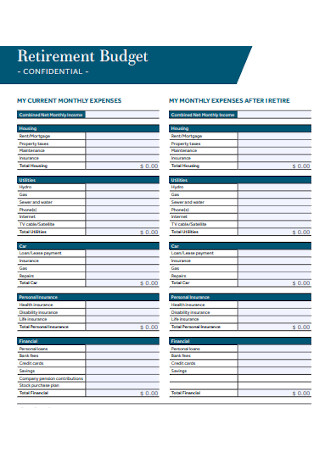

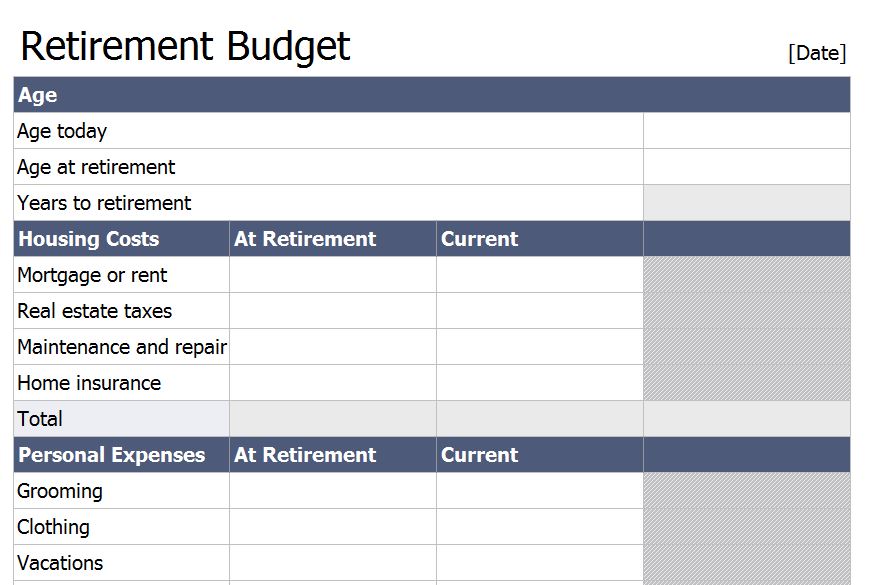

- Housing:

- Mortgage or Rent: Include your monthly mortgage payment or rent.

- Property Taxes: Estimate your annual property taxes.

- Homeowners Insurance: Include your annual homeowners insurance premium.

- Utilities: Estimate your monthly utility costs (electricity, gas, water, trash, internet, cable).

- Home Maintenance and Repairs: Allocate funds for routine maintenance and unexpected repairs.

- Food:

- Groceries: Estimate your weekly or monthly grocery expenses.

- Dining Out: Include the cost of eating at restaurants.

- Transportation:

- Car Payments: Include monthly car payments, if any.

- Car Insurance: Include your annual car insurance premium.

- Gas and Maintenance: Estimate your monthly gas and maintenance costs.

- Public Transportation: Include expenses for buses, trains, or other public transportation.

- Healthcare:

- Health Insurance Premiums: Estimate your monthly health insurance premiums (Medicare, supplemental insurance).

- Out-of-Pocket Medical Expenses: Include estimated costs for doctor visits, medications, and other medical expenses.

- Long-Term Care Insurance: If you have long-term care insurance, include the premiums.

- Personal Care:

- Clothing: Estimate your annual clothing expenses.

- Personal Grooming: Include costs for haircuts, salon services, and other personal grooming needs.

- Entertainment and Recreation:

- Hobbies: Allocate funds for your hobbies and interests.

- Travel: Include expenses for vacations and travel.

- Entertainment: Include costs for movies, concerts, and other entertainment activities.

- Gifts and Donations:

- Gifts: Allocate funds for gifts for family and friends.

- Charitable Donations: Include any charitable donations you plan to make.

- Insurance:

- Life Insurance: Include premiums for life insurance policies.

- Other Insurance: Include premiums for other insurance policies, such as disability insurance.

- Taxes:

- Federal Income Taxes: Estimate your federal income tax liability.

- State Income Taxes: Estimate your state income tax liability.

- Property Taxes (Already Listed Above, but Ensure Accuracy): Double-check your property tax estimate.

- Debt Payments:

- Credit Card Payments: Include minimum monthly payments on credit card debt.

- Loans: Include payments on any outstanding loans.

- Miscellaneous:

- Subscriptions: Include costs for subscriptions (e.g., magazines, streaming services).

- Pet Care: Include expenses for pet food, vet visits, and grooming.

- Other: Include any other expenses not listed above.

Total Estimated Annual Expenses: Sum up all the expense categories listed above.

Phase 3: Budget Analysis and Adjustments

Now, compare your estimated income and expenses.

- Income – Expenses = Surplus/Deficit

If you have a surplus, congratulations! You have more income than expenses. You can use the surplus to increase your savings, pay down debt, or enjoy your retirement even more. If you have a deficit, you need to make adjustments. Consider the following:

- Reduce Expenses: Identify areas where you can cut back on spending. Be realistic and prioritize essential needs over wants.

- Increase Income: Explore opportunities to increase your income, such as part-time work or selling unused assets.

- Adjust Withdrawal Rate: If necessary, adjust your withdrawal rate from retirement accounts. However, be mindful of the long-term sustainability of your savings.

- Downsize: Consider downsizing your home or relocating to a less expensive area.

Phase 4: Regular Review and Updates

Your retirement budget is not a one-time task; it’s an ongoing process. Review and update your budget at least annually, or more frequently if your circumstances change. Consider factors such as:

- Inflation: Adjust your expense estimates to account for inflation.

- Unexpected Expenses: Be prepared for unexpected expenses, such as medical emergencies or home repairs.

- Market Fluctuations: Monitor your investment portfolio and adjust your withdrawal strategy as needed.

- Tax Law Changes: Stay informed about changes in tax laws that could affect your retirement income.

Conclusion

Creating and maintaining a retirement budget is essential for a financially secure and fulfilling retirement. By following this template and regularly reviewing your plan, you can gain control of your finances and enjoy your golden years with peace of mind. Remember to consult with a qualified financial advisor for personalized guidance tailored to your specific circumstances.

320×455 retirement budget samples from www.sample.net

320×455 retirement budget samples from www.sample.net  710×796 plan retirement budget worksheets excel from www.wordtemplatesonline.net

710×796 plan retirement budget worksheets excel from www.wordtemplatesonline.net  1000×1294 retirement budget spreadsheet db excelcom from db-excel.com

1000×1294 retirement budget spreadsheet db excelcom from db-excel.com  1024×744 sample printable budget planner template word excel from bestlettertemplate.com

1024×744 sample printable budget planner template word excel from bestlettertemplate.com  768×1092 retirement budget planner spreadsheet regard retirement budget from db-excel.com

768×1092 retirement budget planner spreadsheet regard retirement budget from db-excel.com  601×778 retirement budget spreadsheet retirement budget spreadsheet from db-excel.com

601×778 retirement budget spreadsheet retirement budget spreadsheet from db-excel.com  390×505 retirement budget worksheet templates from www.template.net

390×505 retirement budget worksheet templates from www.template.net  768×1085 sheet retirement budget planning worksheet thor db excelcom from db-excel.com

768×1085 sheet retirement budget planning worksheet thor db excelcom from db-excel.com  870×585 retirement budget worksheet retirement budget template template haven from templatehaven.com

870×585 retirement budget worksheet retirement budget template template haven from templatehaven.com  770×1024 retirement budget worksheet fill printable fillable blank from www.pdffiller.com

770×1024 retirement budget worksheet fill printable fillable blank from www.pdffiller.com

Budgeting Plan Template For Retirement :

Budgeting Plan Template For Retirement was posted in November 6, 2025 at 8:14 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Budgeting Plan Template For Retirement Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!

Related For Budgeting Plan Template For Retirement

Wedding Budget Plan Template

Crafting Your Dream Day: A Comprehensive Wedding Budget PlanConfidence Building Plan Template

Confidence Building Plan Template Confidence Building Plan Template BuildingMath Lesson Plan Template With Acti

Math Lesson Plan Template & Activities Math Lesson Plan