Emergency Fund Plan Template

Emergency Fund Plan Template: A Comprehensive Guide

An emergency fund is a crucial component of sound personal financial planning. It acts as a financial safety net, providing access to funds to cover unexpected expenses, job loss, or other financial hardships. Without an emergency fund, individuals may resort to high-interest debt, such as credit cards or payday loans, which can quickly escalate into a debt spiral. This template provides a structured approach to establishing and maintaining a robust emergency fund.

I. Assessment and Goal Setting

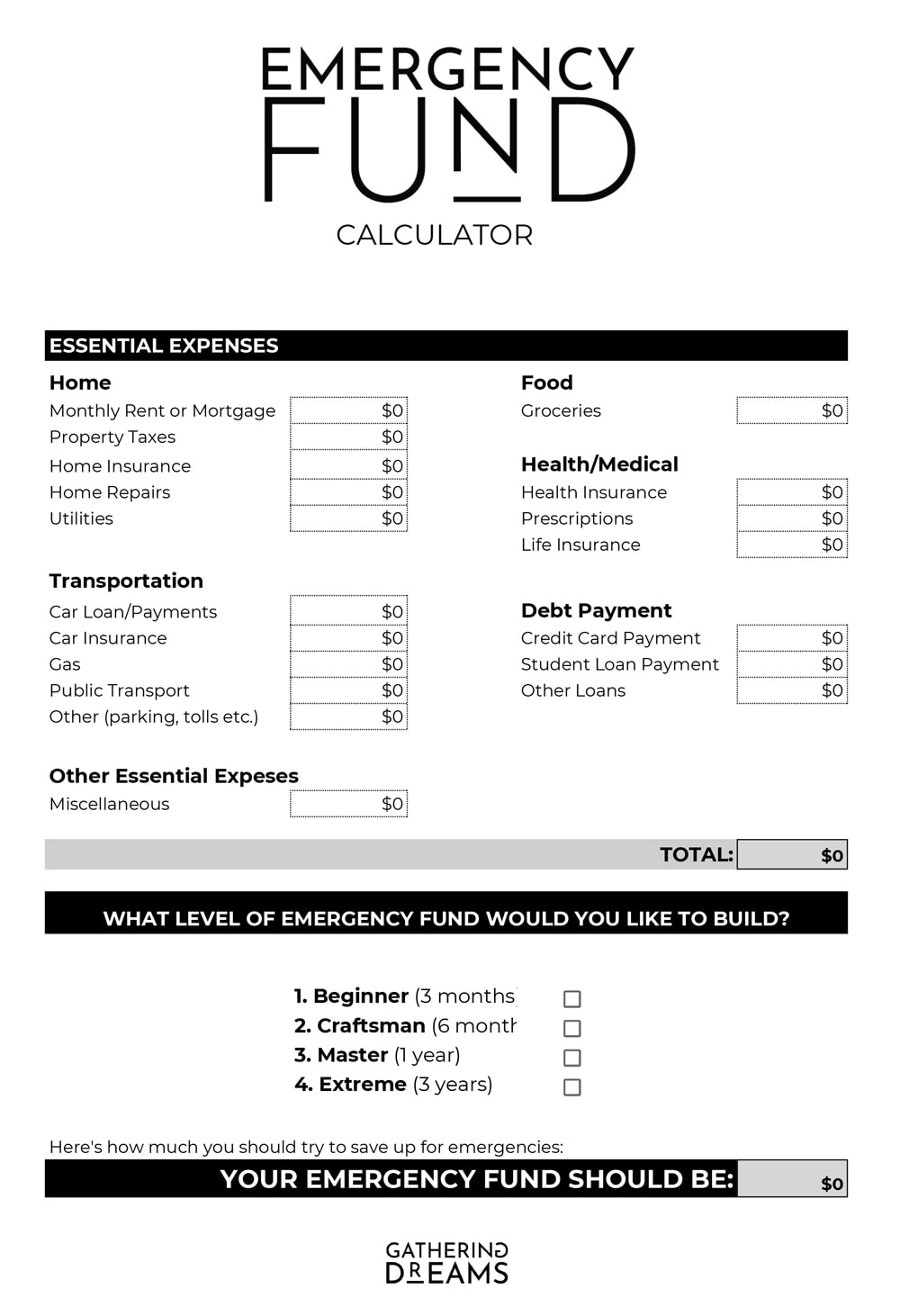

The first step is to assess your current financial situation and define your emergency fund goals. This involves understanding your monthly expenses, income stability, and potential risks. A. Calculate Monthly Expenses: Create a detailed list of all your essential monthly expenses. This includes: * Housing: Rent or mortgage payments, property taxes, homeowner’s insurance. * Utilities: Electricity, gas, water, internet, phone. * Food: Groceries, meals eaten out. * Transportation: Car payments, insurance, gas, public transportation. * Healthcare: Insurance premiums, co-pays, prescription costs. * Debt Payments: Minimum payments on credit cards, loans (student, personal, etc.). * Essential Personal Care: Toiletries, basic clothing. * Childcare: If applicable. Total all these expenses to determine your total monthly essential expenditure. B. Assess Income Stability: Evaluate the stability of your income. Consider: * Job Security: How stable is your job or business? Are there any potential layoffs or business downturns on the horizon? * Income Fluctuations: Does your income vary significantly from month to month (e.g., for freelancers or commission-based employees)? * Alternative Income Sources: Do you have any other sources of income, such as investments or a side hustle? A stable job with a consistent income typically requires a smaller emergency fund compared to an unstable job or fluctuating income. C. Identify Potential Risks: Consider potential unexpected events that could lead to financial strain: * Job Loss: The most common reason for needing an emergency fund. * Medical Expenses: Unexpected medical bills can quickly deplete savings. * Car Repairs: Auto repairs are often expensive and unplanned. * Home Repairs: Appliance breakdowns, plumbing issues, or other home maintenance can be costly. * Natural Disasters: Floods, hurricanes, earthquakes, or other disasters can necessitate unexpected expenses. The more risks you identify, the larger your emergency fund should be. D. Set an Emergency Fund Goal: Based on the assessment above, determine how much you need in your emergency fund. A commonly recommended amount is 3-6 months of essential living expenses. * Conservative Approach (3 Months): Suitable for individuals with stable jobs, low debt, and good health insurance. * Recommended Approach (6 Months): A more comfortable buffer for most individuals, providing ample coverage for unexpected events. * Aggressive Approach (9-12 Months): Ideal for those with unstable jobs, high debt, or significant health concerns. Calculate the target amount: Total Monthly Expenses x Number of Months (3, 6, or 9-12).

II. Savings Plan

Develop a structured plan to build your emergency fund. A. Determine Savings Capacity: Analyze your income and expenses to determine how much you can realistically save each month. * Track Spending: Monitor your spending habits using a budgeting app, spreadsheet, or notebook to identify areas where you can cut back. * Identify Savings Opportunities: Look for areas where you can reduce spending, such as eating out less, cancelling unused subscriptions, or negotiating lower bills. * Calculate Available Funds: Subtract your total monthly expenses from your total monthly income. The remaining amount is your potential savings. B. Set a Monthly Savings Goal: Decide how much you will save each month towards your emergency fund. Aim for a realistic goal that you can consistently achieve. * Prioritize Savings: Treat your emergency fund savings as a non-negotiable expense, similar to rent or utilities. * Automate Savings: Set up automatic transfers from your checking account to your savings account each month. This ensures that you consistently contribute to your emergency fund. C. Create a Timeline: Estimate how long it will take to reach your emergency fund goal based on your monthly savings amount. * Calculate Time to Goal: Divide your total emergency fund goal by your monthly savings amount. This will give you an approximate number of months needed to reach your goal. * Adjust Savings Plan: If the timeline is too long, consider increasing your savings amount by finding additional ways to cut expenses or increase income.

III. Fund Management and Maintenance

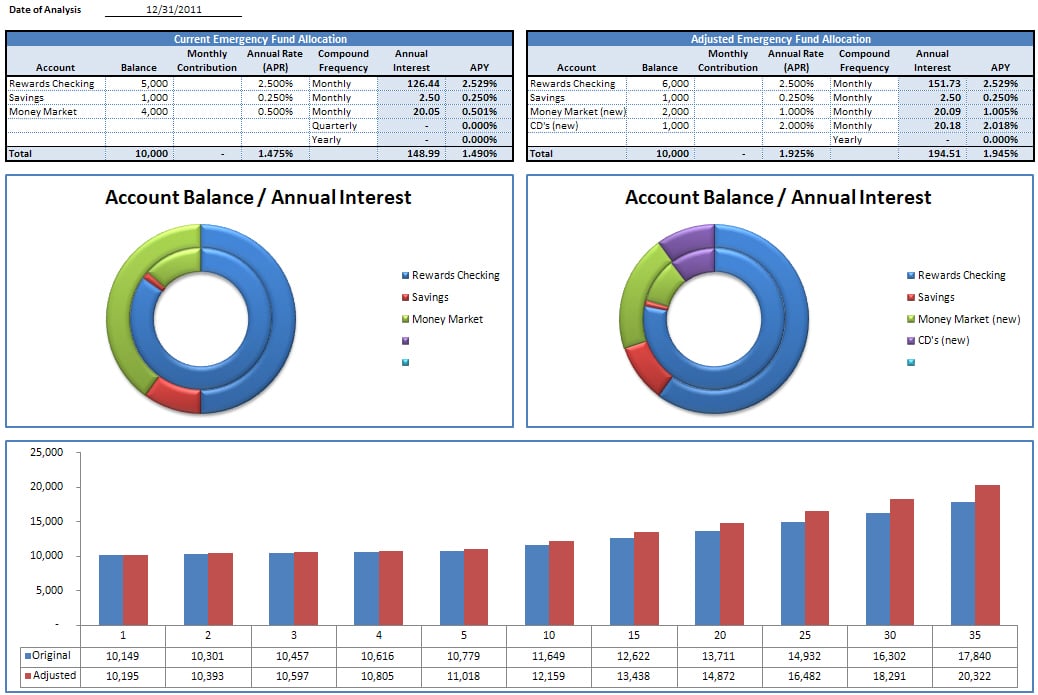

Once your emergency fund is established, it’s essential to manage it effectively and maintain it over time. A. Choose a Safe and Accessible Savings Account: Select a savings account that offers both security and accessibility. * High-Yield Savings Account (HYSA): Offer higher interest rates than traditional savings accounts, helping your emergency fund grow faster. * Money Market Account (MMA): Similar to HYSAs, but may offer check-writing privileges and higher interest rates for larger balances. * Certificate of Deposit (CD): Generally not recommended for emergency funds due to early withdrawal penalties. However, a small portion can be allocated to laddered CDs for slightly higher returns. Ensure that the account is FDIC-insured or NCUA-insured (for credit unions) to protect your funds in case of bank failure. B. Establish Rules for Withdrawal: Define clear guidelines for when and how you can access your emergency fund. * Emergency Only: Reserve the funds for true emergencies, such as job loss, medical expenses, or unexpected home repairs. Avoid using it for non-essential purchases or impulse buys. * Document Withdrawals: Keep a record of all withdrawals, including the date, amount, and reason for the withdrawal. * Replenish the Fund: After using the emergency fund, prioritize replenishing it as quickly as possible. Revert to your savings plan and adjust your budget as needed. C. Regularly Review and Adjust: Periodically review your emergency fund plan to ensure it still meets your needs. * Annual Review: Review your budget, expenses, and potential risks at least once a year. * Adjust Goal Amount: Increase or decrease your emergency fund goal as needed based on changes in your income, expenses, or risk factors. * Re-evaluate Savings Plan: Adjust your monthly savings goal if your income or expenses have changed. * Consider Inflation: Factor in the impact of inflation over time and adjust your goal amount accordingly. By following this comprehensive emergency fund plan template, you can create a strong financial safety net that provides peace of mind and protects you from unexpected financial hardships. Consistent saving, responsible fund management, and regular review are key to maintaining a robust emergency fund that serves its purpose effectively.

736×1104 prepared financial disasters emergency from www.pinterest.com

736×1104 prepared financial disasters emergency from www.pinterest.com  1700×2200 emergency fund challenge printable from www.pinterest.com

1700×2200 emergency fund challenge printable from www.pinterest.com  950×1230 emergency plan fillable templateroller from www.templateroller.com

950×1230 emergency plan fillable templateroller from www.templateroller.com  1200×1200 emergency resource allocation emergency plan template edit from www.template.net

1200×1200 emergency resource allocation emergency plan template edit from www.template.net  696×900 sample emergency plan template word formats page from www.dexform.com

696×900 sample emergency plan template word formats page from www.dexform.com  680×409 create emergency fund template tehkarkheng fiverr from www.fiverr.com

680×409 create emergency fund template tehkarkheng fiverr from www.fiverr.com  1000×1462 emergency fund start from gatheringdreams.com

1000×1462 emergency fund start from gatheringdreams.com  1500×1500 emergency fund world printables from worldofprintables.com

1500×1500 emergency fund world printables from worldofprintables.com  1187×1536 ultimate guide emergency fund financial from www.thefinancialcookbook.com

1187×1536 ultimate guide emergency fund financial from www.thefinancialcookbook.com  763×762 steps build emergency fund budget mom from thebudgetmom.com

763×762 steps build emergency fund budget mom from thebudgetmom.com  1200×2316 emergency plan templates google sheets microsoft excel from slidesdocs.com

1200×2316 emergency plan templates google sheets microsoft excel from slidesdocs.com  736×736 emergency fund emergency fund emergency fund savings plan saving from www.pinterest.com

736×736 emergency fund emergency fund emergency fund savings plan saving from www.pinterest.com  1052×1042 emergency fund printable freedom budget from freedominabudget.com

1052×1042 emergency fund printable freedom budget from freedominabudget.com  1588×1191 emergency fund spreadsheet emergency fund excel dave ramsey from www.etsy.com

1588×1191 emergency fund spreadsheet emergency fund excel dave ramsey from www.etsy.com  1545×2000 cute emergency fund tracker printable templates saturdaygift from www.saturdaygift.com

1545×2000 cute emergency fund tracker printable templates saturdaygift from www.saturdaygift.com  1080×1080 emergency fund printable paper moe from paperbymoe.com

1080×1080 emergency fund printable paper moe from paperbymoe.com  1038×695 excel emergency fund template from www.spreadsheetshoppe.com

1038×695 excel emergency fund template from www.spreadsheetshoppe.com  800×1200 emergency fund printable mom money map from shop.mommoneymap.com

800×1200 emergency fund printable mom money map from shop.mommoneymap.com  2550×2708 emergency fund goal printable emergency fund tracker savings from www.etsy.com

2550×2708 emergency fund goal printable emergency fund tracker savings from www.etsy.com  1545×2000 emergency fund printable instant etsy from www.etsy.com

1545×2000 emergency fund printable instant etsy from www.etsy.com  1056×1048 month emergency fund saving challenge printable freedom budget from freedominabudget.com

1056×1048 month emergency fund saving challenge printable freedom budget from freedominabudget.com  1000×1500 week plan building emergency fund from www.heliodorpress.com

1000×1500 week plan building emergency fund from www.heliodorpress.com  735×1500 starter emergency fund printable from www.pinterest.ca

735×1500 starter emergency fund printable from www.pinterest.ca  1024×830 beginners guide emergency funds mama fish saves from smartmoneymamas.com

1024×830 beginners guide emergency funds mama fish saves from smartmoneymamas.com  1080×1528 printable digital emergency fund template etsy from www.etsy.com

1080×1528 printable digital emergency fund template etsy from www.etsy.com  680×396 emergency fund savings from www.mortgagecalculator.org

680×396 emergency fund savings from www.mortgagecalculator.org  1646×1646 emergency fund mini savings challenge mrsneat from mrsneat.net

1646×1646 emergency fund mini savings challenge mrsneat from mrsneat.net  1024×1024 emergency fund builder printable moderntype designs from moderntype.com

1024×1024 emergency fund builder printable moderntype designs from moderntype.com  1358×1920 freebie printable emergency fund planner artofit from www.artofit.org

1358×1920 freebie printable emergency fund planner artofit from www.artofit.org  1700×2200 emergency fund everhart advisors from everhartadvisors.com

1700×2200 emergency fund everhart advisors from everhartadvisors.com

Emergency Fund Plan Template :

Emergency Fund Plan Template was posted in October 16, 2025 at 8:20 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Emergency Fund Plan Template Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!