Budget Template For Low Income Families

Budget Template for Low-Income Families: A Step-by-Step Guide

Creating and sticking to a budget is crucial for any family, but it’s especially important for low-income families who need to stretch every dollar. A well-designed budget template can provide a roadmap for financial stability, allowing you to prioritize needs, track spending, and ultimately achieve your financial goals. This guide offers a comprehensive budget template tailored specifically for low-income families, complete with explanations and practical tips.

Why is Budgeting Important for Low-Income Families?

Budgeting isn’t just about restricting spending; it’s about empowerment. For low-income families, a budget offers several key benefits:

- Financial Control: A budget allows you to take control of your finances instead of letting your finances control you. It provides visibility into where your money is going and helps you make informed decisions.

- Needs vs. Wants: Budgeting forces you to prioritize essential needs over discretionary wants, ensuring that basic requirements like housing, food, and utilities are met.

- Debt Management: By identifying areas where you can cut back, you can allocate funds towards debt repayment, reducing financial stress and improving your credit score.

- Savings Goals: Even small savings can accumulate over time. A budget helps you identify opportunities to save for emergencies, future education, or other important goals.

- Reduced Stress: Knowing where your money is going and having a plan can significantly reduce financial anxiety and improve your overall well-being.

The Low-Income Family Budget Template: A Detailed Breakdown

This budget template is designed to be simple and adaptable to your specific circumstances. Feel free to modify it to fit your family’s needs.

Step 1: Calculate Your Monthly Income

This is the foundation of your budget. Include all sources of income, such as:

- Net Paycheck(s): Your income after taxes and other deductions. This is the most important number to focus on.

- Government Assistance: Include benefits like SNAP (Supplemental Nutrition Assistance Program), TANF (Temporary Assistance for Needy Families), WIC (Women, Infants, and Children), and housing assistance.

- Child Support/Alimony: Any regular payments received for child support or alimony.

- Self-Employment Income: If you have a side hustle or are self-employed, calculate your average monthly net income (after deducting business expenses).

- Other Income: Include any other regular sources of income, such as disability payments, social security benefits, or investment income.

Example:

- Net Paycheck (Spouse 1): $1200

- Net Paycheck (Spouse 2): $800

- SNAP Benefits: $200

- Child Support: $100

- Total Monthly Income: $2300

Step 2: List Your Monthly Expenses

This is where you meticulously track where your money is going. It’s crucial to be honest and thorough. Categorize your expenses as follows:

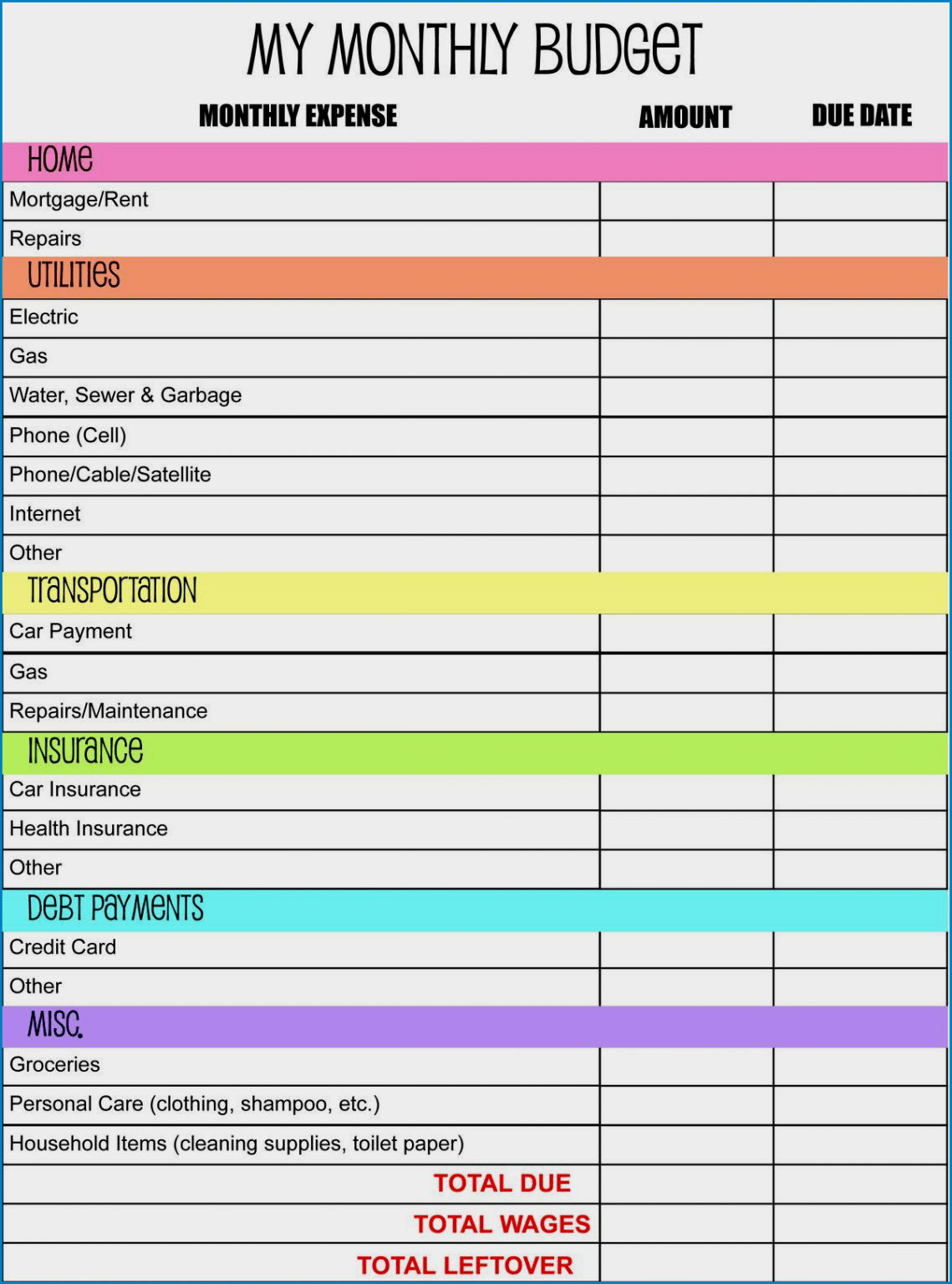

A. Housing

- Rent or Mortgage: Your monthly housing payment.

- Property Taxes (if applicable): If you own your home.

- Homeowners Insurance (if applicable): Required if you own your home.

- HOA Fees (if applicable): If you live in a community with a homeowners association.

B. Utilities

- Electricity: Your monthly electric bill.

- Gas: Your monthly gas bill (if applicable).

- Water/Sewer: Your monthly water and sewer bill.

- Trash/Recycling: Your monthly trash and recycling bill.

- Phone: Your monthly phone bill (consider a lower-cost plan).

- Internet: Your monthly internet bill (shop around for the best deals).

C. Food

- Groceries: Your weekly grocery budget multiplied by four. Prioritize meal planning and cooking at home to save money.

- Eating Out: Try to minimize eating out. This is often a significant source of unnecessary spending.

D. Transportation

- Car Payment: Your monthly car payment (if applicable).

- Car Insurance: Your monthly car insurance premium.

- Gasoline: Your monthly gas expense.

- Public Transportation: Your monthly bus or train fare.

- Car Maintenance: Allocate a small amount each month for car repairs and maintenance.

E. Healthcare

- Health Insurance Premium: Your monthly health insurance premium.

- Doctor’s Visits/Copays: Estimate your average monthly cost for doctor’s visits and copays.

- Medications: Include the cost of any prescription medications.

F. Childcare

- Daycare/Preschool: Your monthly childcare expenses.

G. Debt Payments

- Credit Card Payments: List each credit card payment and the amount.

- Student Loan Payments: Your monthly student loan payment.

- Personal Loan Payments: Your monthly personal loan payment.

H. Personal Care

- Toiletries: Soap, shampoo, toothpaste, etc.

- Haircuts: Costs for haircuts.

I. Entertainment

- Streaming Services: Netflix, Hulu, etc. (consider canceling or sharing subscriptions).

- Other Entertainment: Movies, concerts, etc. (try to find free or low-cost alternatives).

J. Miscellaneous

- Clothing: Allocate a small amount for clothing purchases.

- Household Supplies: Cleaning supplies, etc.

- Gifts: Budget for birthdays and holidays.

- Other: Any other recurring expenses.

Example (Partial):

- Rent: $800

- Electricity: $150

- Groceries: $400

- Car Insurance: $100

- Credit Card Payment: $50

Step 3: Total Your Expenses

Add up all the expenses from Step 2 to determine your total monthly expenses.

Step 4: Calculate Your Net Income

Subtract your total monthly expenses (Step 3) from your total monthly income (Step 1). This will give you your net income (either a surplus or a deficit).

Example:

- Total Monthly Income: $2300

- Total Monthly Expenses: $2100

- Net Income: $200

Step 5: Analyze and Adjust Your Budget

This is the crucial step where you analyze your budget and make adjustments to ensure you’re meeting your financial goals.

- Surplus: If you have a surplus (positive net income), decide how to allocate it. Consider putting it towards savings, debt repayment, or a specific financial goal.

- Deficit: If you have a deficit (negative net income), you need to make immediate adjustments to your spending. Identify areas where you can cut back. Some strategies include:

- Reducing Groceries: Plan meals, shop with a list, use coupons, and buy in bulk.

- Lowering Utility Bills: Conserve energy and water.

- Cutting Entertainment: Find free or low-cost entertainment options.

- Negotiating Bills: Call your service providers (phone, internet, insurance) to negotiate lower rates.

- Reducing Transportation Costs: Carpool, use public transportation, or walk/bike when possible.

- Eliminating Non-Essential Expenses: Identify and cut out unnecessary spending.

Step 6: Track Your Spending

Tracking your spending is essential to ensure you’re sticking to your budget. Use a notebook, spreadsheet, or budgeting app to track every dollar you spend. Regularly review your spending to identify areas where you might be overspending.

Step 7: Review and Adjust Regularly

Your budget is not a static document. It should be reviewed and adjusted regularly (at least monthly) to reflect changes in your income, expenses, and financial goals. Life events like job changes, medical expenses, or unexpected repairs may require adjustments to your budget.

Tips for Success

- Be Realistic: Create a budget that is realistic and achievable. Don’t try to cut back too drastically, as this can lead to frustration and failure.

- Be Consistent: Stick to your budget as closely as possible. Consistency is key to achieving your financial goals.

- Be Patient: It takes time to develop good budgeting habits. Don’t get discouraged if you slip up. Just get back on track as quickly as possible.

- Seek Support: Talk to a financial advisor or counselor for personalized guidance. Many non-profit organizations offer free or low-cost financial advice to low-income families.

- Celebrate Small Wins: Acknowledge and celebrate your progress, no matter how small. This will help you stay motivated and committed to your financial goals.

Conclusion

Creating and maintaining a budget is a powerful tool for low-income families. By following this budget template and incorporating the tips provided, you can gain control of your finances, reduce stress, and work towards a more secure financial future. Remember that budgeting is a journey, not a destination. Be patient, persistent, and celebrate your successes along the way.

680×826 family budget templates word excel from www.template.net

680×826 family budget templates word excel from www.template.net  329×425 budgeting worksheets income families lovetoknow from save.lovetoknow.com

329×425 budgeting worksheets income families lovetoknow from save.lovetoknow.com  1480×2100 printable colored family budget template from onplanners.com

1480×2100 printable colored family budget template from onplanners.com  474×576 family budget templates word excel formats samples from www.wordpdftemplates.com

474×576 family budget templates word excel formats samples from www.wordpdftemplates.com  378×629 reader question budgeting tips income families canadian from canadianbudgetbinder.com

378×629 reader question budgeting tips income families canadian from canadianbudgetbinder.com  1139×1536 printable family budget template from www.templateral.com

1139×1536 printable family budget template from www.templateral.com  377×1024 budgeting income families from www.moneysense.ca

377×1024 budgeting income families from www.moneysense.ca  796×1034 printable budget templates absolutely crush finances from mamaandmoney.com

796×1034 printable budget templates absolutely crush finances from mamaandmoney.com  768×694 sample printable budget planner template word excel from bestlettertemplate.com

768×694 sample printable budget planner template word excel from bestlettertemplate.com

Budget Template For Low Income Families :

Budget Template For Low Income Families was posted in September 26, 2025 at 4:20 pm. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Budget Template For Low Income Families Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!

Related For Budget Template For Low Income Families

Free Dream Vacation Budget Template

Free Dream Vacation Budget Template PDF Format Free MoneySingle Income Household Budget

Single Income, Solid Budget: A Guide to Financial Security

Sample Excel Budget Template

Sample Excel Budget Template Printable Budget Planner Organizer Monthly