Personal Financial Plan Template

Crafting Your Financial Future: A Guide to Using a Personal Financial Plan Template

Planning for your financial future can feel overwhelming. Where do you start? How do you prioritize your goals? A well-structured personal financial plan template can be your roadmap, guiding you toward achieving your financial aspirations. This guide will walk you through the key components of a comprehensive personal financial plan template and how to effectively utilize it.

Understanding the Purpose of a Financial Plan Template

A financial plan template provides a structured framework for organizing your financial information, setting goals, and developing strategies to reach those goals. It’s not a one-size-fits-all solution, but a customizable tool that you can adapt to your specific circumstances and objectives. The primary purpose is to provide clarity, direction, and control over your financial life.

Key Components of a Personal Financial Plan Template

A robust financial plan template typically includes the following sections:

1. Executive Summary

This section provides a brief overview of your current financial situation and your primary financial goals. It’s a concise summary of the entire plan and serves as a quick reference point. It might include key metrics like your net worth, debt levels, and savings rates.

2. Financial Goals

This is where you define what you want to achieve financially. Be specific, measurable, achievable, relevant, and time-bound (SMART goals). Examples include: * **Short-Term Goals (1-3 years):** Paying off credit card debt, building an emergency fund, saving for a down payment on a car. * **Medium-Term Goals (3-10 years):** Saving for a house, paying off student loans, funding a child’s education. * **Long-Term Goals (10+ years):** Retirement planning, wealth accumulation, legacy planning. For each goal, specify the target amount, the timeframe for achieving it, and the strategies you’ll use. For instance, “Save $10,000 for a down payment on a car within 2 years by saving $417 per month.”

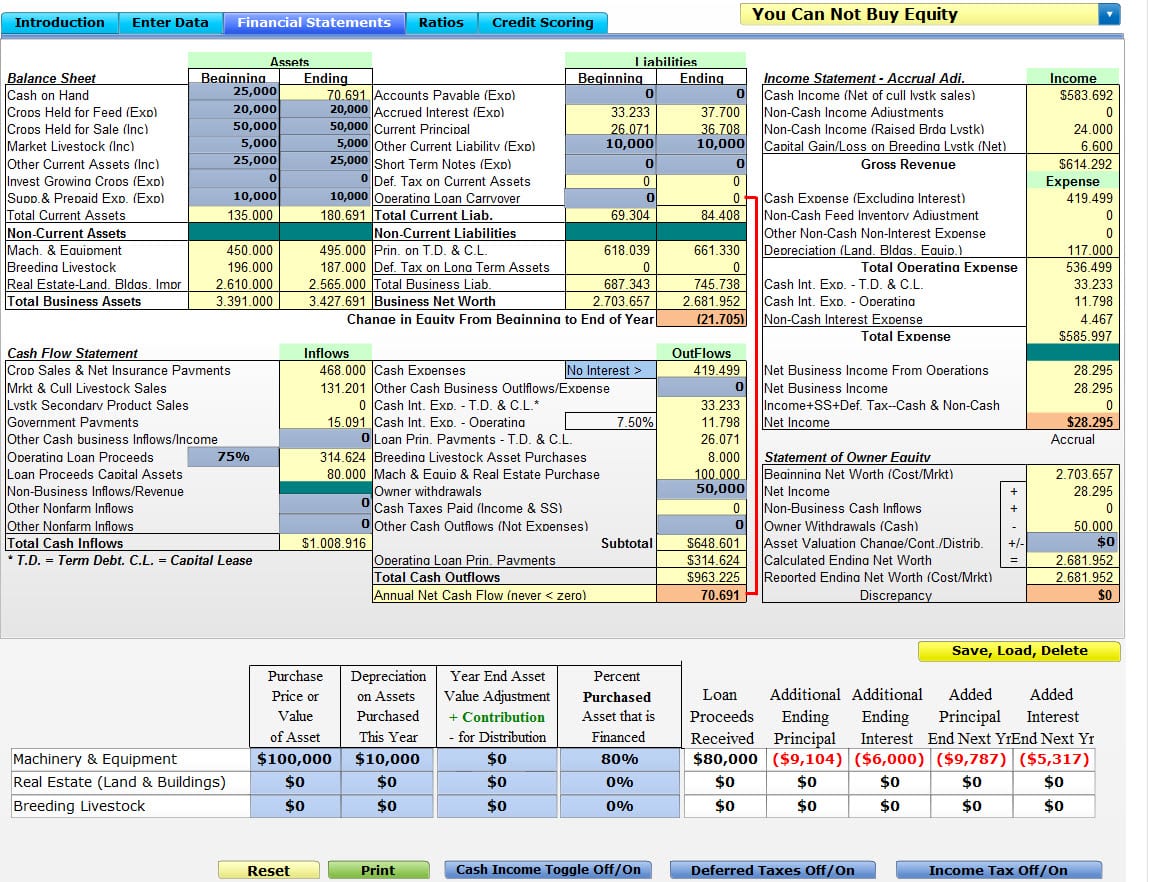

3. Current Financial Situation

This section provides a snapshot of your current financial health. It typically includes: * **Balance Sheet:** A summary of your assets (what you own) and liabilities (what you owe). * **Assets:** Cash, savings accounts, investments (stocks, bonds, mutual funds), real estate, personal property. * **Liabilities:** Credit card debt, student loans, mortgage, auto loans. * **Net Worth:** Calculated as Assets – Liabilities. This is a key indicator of your overall financial health. * **Income Statement:** A summary of your income and expenses over a specific period (e.g., monthly or annually). * **Income:** Salary, wages, investment income, business income, other sources of income. * **Expenses:** Housing, transportation, food, utilities, entertainment, debt payments, insurance. * **Cash Flow:** Calculated as Income – Expenses. This indicates whether you have a surplus or deficit each month.

4. Budgeting and Cash Flow Management

This section outlines how you will manage your income and expenses to achieve your financial goals. It typically involves: * **Creating a Budget:** Allocating your income to different expense categories based on your priorities. * **Tracking Expenses:** Monitoring your actual spending to identify areas where you can save money. * **Identifying Savings Opportunities:** Finding ways to reduce expenses and increase savings. Common budgeting methods include the 50/30/20 rule (50% needs, 30% wants, 20% savings and debt repayment) or zero-based budgeting (allocating every dollar of income).

5. Debt Management

This section focuses on strategies for managing and reducing your debt. It might include: * **Debt Consolidation:** Combining multiple debts into a single loan with a lower interest rate. * **Debt Snowball Method:** Paying off the smallest debt first, regardless of interest rate, for psychological motivation. * **Debt Avalanche Method:** Paying off the debt with the highest interest rate first to minimize overall interest costs. The template should help you prioritize debts and develop a plan to pay them off systematically.

6. Investment Planning

This section outlines your investment strategy based on your risk tolerance, time horizon, and financial goals. It typically includes: * **Asset Allocation:** Deciding how to distribute your investments among different asset classes (e.g., stocks, bonds, real estate). * **Investment Selection:** Choosing specific investments within each asset class (e.g., individual stocks, mutual funds, ETFs). * **Diversification:** Spreading your investments across different assets to reduce risk. Your investment strategy should be aligned with your long-term goals, such as retirement planning. Consider factors like your age, income, and comfort level with risk.

7. Retirement Planning

This section focuses on saving and investing for retirement. It typically includes: * **Estimating Retirement Expenses:** Determining how much money you will need to cover your living expenses in retirement. * **Calculating Retirement Savings Needs:** Projecting how much you need to save to reach your retirement goal. * **Maximizing Retirement Savings:** Taking advantage of tax-advantaged retirement accounts (e.g., 401(k), IRA). This section should also consider potential sources of retirement income, such as Social Security and pensions.

8. Insurance Planning

This section reviews your insurance coverage to ensure you have adequate protection against financial risks. It typically includes: * **Life Insurance:** Providing financial support to your dependents in the event of your death. * **Health Insurance:** Covering medical expenses. * **Disability Insurance:** Replacing lost income if you become disabled and unable to work. * **Homeowners/Renters Insurance:** Protecting your home and personal property from damage or loss. * **Auto Insurance:** Covering damages and liabilities related to auto accidents. Ensure your insurance policies provide sufficient coverage to protect your assets and loved ones.

9. Estate Planning

This section focuses on planning for the distribution of your assets after your death. It typically includes: * **Will:** A legal document specifying how you want your assets to be distributed. * **Trust:** A legal arrangement that holds assets for the benefit of beneficiaries. * **Power of Attorney:** A legal document authorizing someone to act on your behalf if you become incapacitated. * **Healthcare Directive:** A legal document outlining your wishes regarding medical treatment. Estate planning ensures that your assets are distributed according to your wishes and minimizes potential estate taxes.

10. Action Plan and Review

This section outlines the steps you need to take to implement your financial plan and establishes a schedule for reviewing and updating it. It typically includes: * **Specific Action Items:** Detailing the tasks you need to complete to achieve your financial goals. * **Timelines:** Setting deadlines for completing each action item. * **Regular Review:** Scheduling periodic reviews (e.g., quarterly or annually) to monitor your progress and make adjustments as needed. Your financial plan is not a static document. It should be reviewed and updated regularly to reflect changes in your circumstances, goals, and the economic environment.

Tips for Using a Financial Plan Template Effectively

* **Be Honest and Realistic:** Provide accurate information about your income, expenses, assets, and liabilities. * **Customize the Template:** Adapt the template to your specific needs and goals. * **Seek Professional Advice:** Consult with a financial advisor if you need help developing your plan or making investment decisions. * **Stay Disciplined:** Stick to your budget and savings plan as much as possible. * **Track Your Progress:** Monitor your progress regularly and make adjustments as needed. By using a personal financial plan template and following these tips, you can take control of your financial future and work towards achieving your dreams. Remember, financial planning is an ongoing process, not a one-time event. Regularly review and update your plan to ensure it remains aligned with your goals and circumstances.

1024×1446 personal financial plans templates format templatenet from www.template.net

1024×1446 personal financial plans templates format templatenet from www.template.net  585×651 financial plan template word excel documents from www.template.net

585×651 financial plan template word excel documents from www.template.net  1254×812 personal financial planning template sampletemplatess from www.sampletemplatess.com

1254×812 personal financial planning template sampletemplatess from www.sampletemplatess.com  1149×882 sample personal financial plan template excelxocom from excelxo.com

1149×882 sample personal financial plan template excelxocom from excelxo.com  1280×965 simple personal financial plan template resourcesaver from db-excel.com

1280×965 simple personal financial plan template resourcesaver from db-excel.com  1255×970 financial plan template spreadsheet templates business finance from db-excel.com

1255×970 financial plan template spreadsheet templates business finance from db-excel.com  2036×2500 professional financial plan templates personal business from templatelab.com

2036×2500 professional financial plan templates personal business from templatelab.com  585×685 sample personal financial plan template classles democracy from classlesdemocracy.blogspot.com

585×685 sample personal financial plan template classles democracy from classlesdemocracy.blogspot.com  474×498 sample financial plan templates ms word excel from www.sampletemplates.com

474×498 sample financial plan templates ms word excel from www.sampletemplates.com  650×975 personal financial plan manage money pro from millionairemob.com

650×975 personal financial plan manage money pro from millionairemob.com

Personal Financial Plan Template :

Personal Financial Plan Template was posted in June 27, 2025 at 1:04 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Personal Financial Plan Template Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!