Budgeting Plan Template For Low-income Households

Budgeting Plan Template for Low-Income Households

Managing finances on a low income can feel overwhelming, but with a structured budget, you can gain control, prioritize needs, and even start saving. This budgeting plan template offers a practical approach to help low-income households track income, expenses, and identify areas for improvement. Remember, consistency is key to success.

I. Understanding Your Income

The first step is to accurately determine your total monthly income. This includes all sources of money coming into your household.

A. List All Income Sources:

- Wages/Salary (after taxes): Net pay from your job(s). Note the actual amount deposited into your bank account after deductions.

- Government Assistance: Include amounts received from SNAP (Supplemental Nutrition Assistance Program), TANF (Temporary Assistance for Needy Families), unemployment benefits, disability payments (SSI/SSDI), housing assistance (Section 8), or other public assistance programs. Be precise with the amounts.

- Child Support/Alimony: If you receive these payments, include the consistent monthly amount.

- Part-Time Income/Side Hustles: List any earnings from gig work, freelance jobs, selling items, or other income-generating activities. Try to average inconsistent earnings over a few months to arrive at a realistic monthly figure.

- Investment Income: Include any dividends, interest, or other returns from investments, however small.

- Other Income: Include any other regular income sources, such as contributions from family members or occasional gifts intended for recurring use (e.g., a relative helps with groceries each month).

B. Calculate Total Monthly Income:

Sum up all the amounts from the income sources listed above. This is your total monthly income available for budgeting.

II. Tracking Your Expenses

The next step is to meticulously track where your money is going. This is often the most eye-opening part of budgeting.

A. Differentiate Between Fixed and Variable Expenses:

Understanding the difference between these two types of expenses is crucial for effective budgeting.

- Fixed Expenses: These are expenses that remain relatively consistent each month, such as rent/mortgage, loan payments, insurance premiums, and set subscription fees.

- Variable Expenses: These expenses fluctuate from month to month, such as groceries, utilities, transportation, entertainment, and clothing.

B. List and Categorize Your Expenses:

Create a detailed list of all your monthly expenses, categorized for clarity.

- Housing:

- Rent/Mortgage

- Property Taxes (if applicable)

- Homeowner’s Insurance (if applicable)

- HOA Fees (if applicable)

- Repairs & Maintenance

- Utilities:

- Electricity

- Gas

- Water/Sewer/Trash

- Internet

- Phone (Cell & Landline)

- Food:

- Groceries

- Eating Out

- Transportation:

- Car Payment

- Car Insurance

- Gasoline

- Public Transportation

- Car Repairs & Maintenance

- Healthcare:

- Health Insurance Premiums

- Doctor’s Visits (Co-pays)

- Prescriptions

- Over-the-Counter Medications

- Debt Payments:

- Credit Card Payments (minimum payments)

- Student Loan Payments

- Personal Loan Payments

- Medical Debt Payments

- Personal Care:

- Toiletries

- Haircuts

- Other Personal Grooming

- Clothing:

- New Clothing

- Laundry/Dry Cleaning

- Entertainment:

- Movies

- Concerts

- Streaming Services

- Hobbies

- Childcare:

- Daycare

- Babysitting

- Education:

- Tuition (if applicable)

- School Supplies

- Insurance (Other):

- Life Insurance

- Disability Insurance

- Miscellaneous:

- Gifts

- Pet Care

- Subscriptions

- Bank Fees

- Other Unexpected Expenses

C. Use Tracking Methods:

- Notebook/Spreadsheet: A simple notebook or spreadsheet can be effective for manually tracking expenses.

- Budgeting Apps: Mint, YNAB (You Need a Budget), Personal Capital, and Goodbudget offer free or low-cost options for tracking and categorizing expenses automatically.

- Bank Statements: Review your bank statements and credit card statements to identify where your money is going.

- Receipts: Save receipts for a week or two to get a clear picture of your spending habits.

D. Calculate Total Monthly Expenses:

Sum up all the amounts from each expense category. This is your total monthly spending.

III. Creating Your Budget and Identifying Areas for Improvement

A. Compare Income and Expenses:

Subtract your total monthly expenses from your total monthly income. The result will either be a surplus (positive number) or a deficit (negative number).

- Surplus: You are spending less than you earn. This is a good position to be in, allowing you to save and invest.

- Deficit: You are spending more than you earn. This requires immediate attention and adjustments to your spending habits.

B. Prioritize Needs vs. Wants:

Carefully review your expense list and distinguish between essential needs and discretionary wants. Needs are things necessary for survival and well-being, while wants are things you can live without.

- Needs: Housing, utilities, basic food, transportation to work, healthcare.

- Wants: Eating out, entertainment, expensive clothing, subscriptions you don’t use, etc.

C. Identify Areas to Cut Back:

Focus on reducing spending in the “wants” category first. Even small cuts can make a significant difference over time.

- Food: Meal planning, cooking at home, reducing eating out, utilizing coupons and discounts, buying in bulk (when cost-effective).

- Transportation: Using public transportation, carpooling, biking or walking when possible, reducing unnecessary trips.

- Entertainment: Finding free or low-cost activities, canceling unnecessary subscriptions, borrowing books and movies from the library.

- Utilities: Conserving energy and water, unplugging electronics when not in use, adjusting thermostat settings.

- Other: Negotiating bills, finding free alternatives to paid services, delaying non-essential purchases.

D. Allocate Funds for Savings (Even Small Amounts):

Even when on a low income, saving is still possible and crucial for financial security. Start with small, achievable goals.

- Emergency Fund: Aim to save at least $500-$1000 for unexpected expenses.

- Specific Goals: Save for a down payment, a vacation, or other desired purchases.

- Automatic Transfers: Set up automatic transfers from your checking account to a savings account each month.

E. Regularly Review and Adjust Your Budget:

Your budget is not a static document. It should be reviewed and adjusted regularly to reflect changes in your income, expenses, and financial goals. Aim to review your budget at least once a month.

IV. Tips for Success

- Be Realistic: Create a budget that you can actually stick to. Don’t set unrealistic goals that will lead to discouragement.

- Be Consistent: Track your spending consistently and make adjustments as needed.

- Automate: Automate bill payments and savings transfers to avoid late fees and ensure consistent savings.

- Seek Help: If you are struggling to manage your finances, consider seeking help from a financial counselor or non-profit organization. They can provide personalized guidance and support.

- Celebrate Small Wins: Acknowledge and celebrate your progress along the way to stay motivated.

By following this budgeting plan template and staying committed to your financial goals, you can take control of your finances, reduce stress, and build a more secure future, even on a low income.

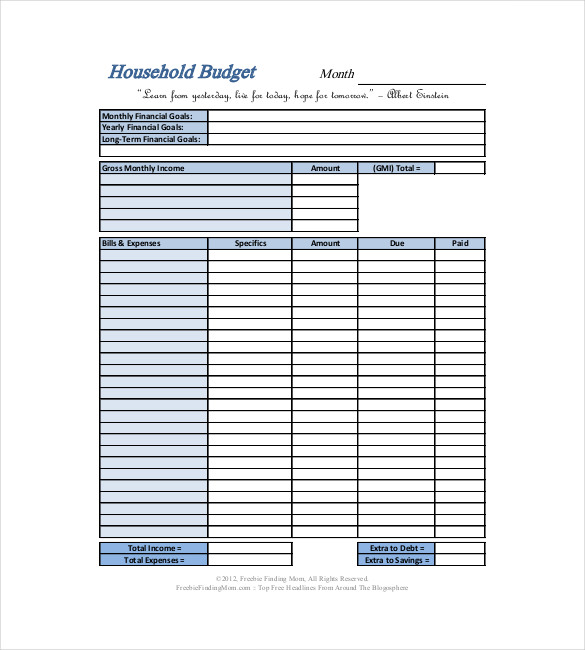

585×650 household budget template from templatedocs.net

585×650 household budget template from templatedocs.net  1322×844 household budget template xls kb pages from www.speedytemplate.com

1322×844 household budget template xls kb pages from www.speedytemplate.com  600×730 household budget template budget template tips from www.pinterest.com

600×730 household budget template budget template tips from www.pinterest.com  1480×2100 printable simple household budget from onplanners.com

1480×2100 printable simple household budget from onplanners.com  843×1500 easy household budget template artofit from www.artofit.org

843×1500 easy household budget template artofit from www.artofit.org  736×952 budgeting budget template household budget template from www.pinterest.com

736×952 budgeting budget template household budget template from www.pinterest.com  987×1278 sample household budget template sampletemplatess sampletemplatess from www.sampletemplatess.com

987×1278 sample household budget template sampletemplatess sampletemplatess from www.sampletemplatess.com  700×990 personalize flat linear budget overview planner design from wepik.com

700×990 personalize flat linear budget overview planner design from wepik.com  600×840 household budget template household budget template family from www.pinterest.com

600×840 household budget template household budget template family from www.pinterest.com  1226×735 easy household budget template dremelmicro from dremelmicro.com

1226×735 easy household budget template dremelmicro from dremelmicro.com  600×704 household budget samples google docs google sheets from www.sampletemplates.com

600×704 household budget samples google docs google sheets from www.sampletemplates.com  1979×1285 simple budget plan template sampletemplatess sampletemplatess from www.sampletemplatess.com

1979×1285 simple budget plan template sampletemplatess sampletemplatess from www.sampletemplatess.com  475×578 income budgeting individuals income budgeting from www.pinterest.com

475×578 income budgeting individuals income budgeting from www.pinterest.com  1024×510 budget templates ms wordexcel google docs from www.templatehub.org

1024×510 budget templates ms wordexcel google docs from www.templatehub.org  816×1056 household budget template printable from www.bizzlibrary.com

816×1056 household budget template printable from www.bizzlibrary.com  585×630 household budget templates printable word excel samples from www.wordstemplates.org

585×630 household budget templates printable word excel samples from www.wordstemplates.org  702×908 printable household budget template from www.templateral.com

702×908 printable household budget template from www.templateral.com  1140×1140 budget template printable income budget printable budget template from www.etsy.com

1140×1140 budget template printable income budget printable budget template from www.etsy.com  735×1102 income budget beginner printable budget worksheet budgeting from budgeting-worksheets.com

735×1102 income budget beginner printable budget worksheet budgeting from budgeting-worksheets.com  637×616 simple household budget template template haven from templatehaven.com

637×616 simple household budget template template haven from templatehaven.com  768×694 sample printable budget planner template word excel from bestlettertemplate.com

768×694 sample printable budget planner template word excel from bestlettertemplate.com  796×1034 printable budget templates absolutely crush finances from mamaandmoney.com

796×1034 printable budget templates absolutely crush finances from mamaandmoney.com  1080×721 basic household budget template customisable etsy from www.etsy.com

1080×721 basic household budget template customisable etsy from www.etsy.com  1870×2420 basic monthly budget template from mungfali.com

1870×2420 basic monthly budget template from mungfali.com  329×425 budgeting worksheets income families lovetoknow from save.lovetoknow.com

329×425 budgeting worksheets income families lovetoknow from save.lovetoknow.com  770×1155 monthly income budgeting etsy from www.etsy.com

770×1155 monthly income budgeting etsy from www.etsy.com  795×1124 simple household budget template hdlinda from hdlinda.weebly.com

795×1124 simple household budget template hdlinda from hdlinda.weebly.com  1000×1500 income budget worksheet from liveworksheetbyearth.netlify.app

1000×1500 income budget worksheet from liveworksheetbyearth.netlify.app  1480×2100 basic household budget template from lesboucans.com

1480×2100 basic household budget template from lesboucans.com

Budgeting Plan Template For Low-income Households :

Budgeting Plan Template For Low-income Households was posted in June 23, 2025 at 8:46 am. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Budgeting Plan Template For Low-income Households Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by SampleTemplates123... Thanks again! If you have any DMCA issues on this post, please contact us!